Physical AI and the Coming Industrial Up-Cycle: A Strategic Outlook

As labor shortages intensify, a technology-driven transformation is reshaping industrial automation. This shift, termed the “Physical AI” up-cycle, promises to redefine productivity through smarter, more adaptable robotic systems. According to Morten Paulsen of CLSA, these trends will push U.S. robot shipments toward record levels in 2026.

Global Momentum Behind Physical AI

The concept of Physical AI gained significant traction in 2025. Initially focused on humanoid robots, the market’s understanding expanded dramatically. A pivotal moment was SoftBank’s acquisition of ABB Robotics. Consequently, investors recognized that AI’s physical applications extend far beyond human-like forms to encompass all automated equipment.

Diverging Regional Investment Focus

Investor enthusiasm varies globally. In China and Singapore, attention remains heavily concentrated on the humanoid robot segment. However, markets like Japan, the U.S., and Europe take a broader view. Therefore, they are investing across the entire industrial automation ecosystem, from collaborative robots to autonomous mobile systems.

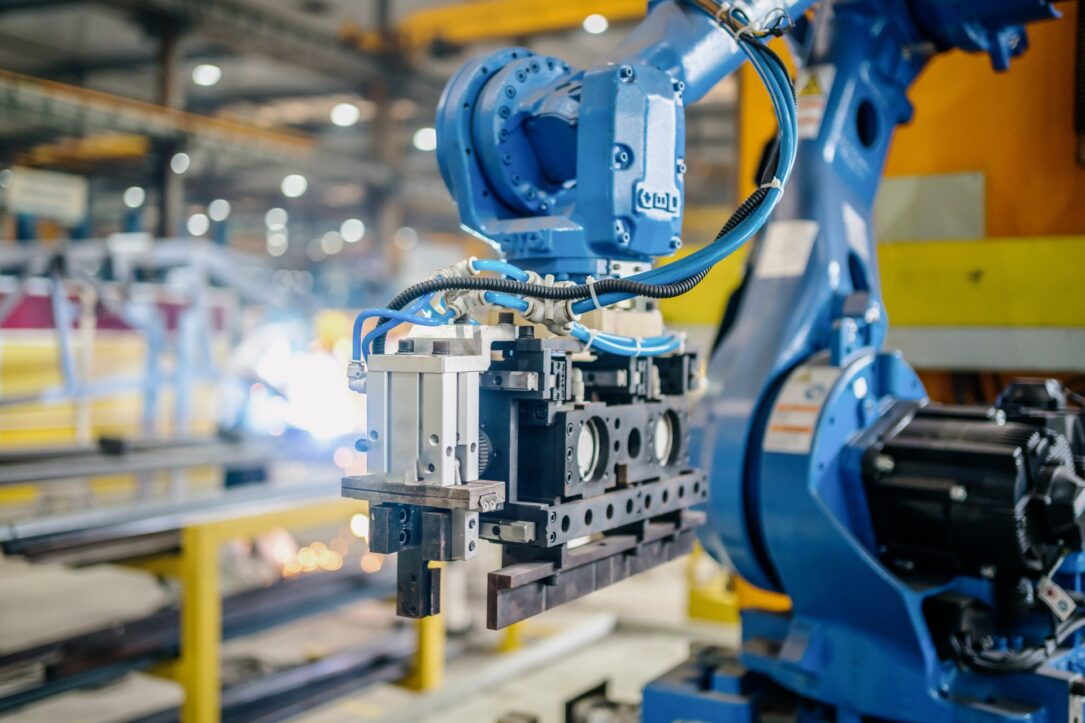

The Critical Challenge: Robotic Dexterity

While robots have gained vision, mobility, and language understanding, a key limitation persists. Paulsen identifies advanced end-effectors, or “hands,” as the next frontier. Tactile sensing and refined manipulation are crucial for unlocking more complex applications. This area represents a significant and underappreciated development focus for 2026.

Labor Shortages: A Primary Automation Catalyst

Persistent demographic challenges are creating a massive workforce gap in U.S. manufacturing. Historical data shows a 94% correlation between job openings and subsequent robot installations. Although the post-COVID gap has narrowed, demand remains strong. With roughly 400,000 manufacturing job openings, we can anticipate nearly 40,000 robot shipments in 2026. This would mark a 30% annual growth rate.

China’s Dual Role: Market Leader and Competitor

China continues to dominate as the world’s largest robot market. Despite geopolitical tensions, demand in automotive and electronics sectors stayed resilient in 2025. Foreign firms like Fanuc and Yaskawa even reported solid growth there. While Chinese manufacturers are expanding abroad, they face high barriers in established markets. These include strict safety certifications and the need for proven system reliability, where incumbent leaders still hold significant advantage.

Underappreciated Trends and Future Frontiers

The market often overlooks robotics’ potential beyond human tasks. Paulsen highlights groundbreaking areas like medical nano-robots. Furthermore, he advocates for designing robots tailored to specific, unmet industrial needs—such as rare earth mining. This mindset opens virtually unlimited application potential, moving automation into completely new domains.

Navigating the Current Tech-Driven Up-Cycle

After a volatile 2025, the industrial automation sector is now firmly in an up-cycle. Initially driven by technology adoption rather than traditional capital expenditure, this cycle is expected to broaden. Automotive sector investment is projected to rebound later in 2026. The result will be a sustained, though more measured, growth period compared to the post-pandemic surge.

Strategic Implications for Industrial Automation

This transition necessitates a strategic shift. Integrators and manufacturers must look beyond simple labor replacement. The focus should be on integrating AI for adaptive control, investing in advanced sensing like tactile feedback, and developing robots for tasks impossible for humans. Success will depend on creating robust, reliable systems where every component, from the PLC to the end-effector, is optimized.

Application Scenario: Agile Assembly Line

A consumer electronics manufacturer faces frequent product line changes. By deploying AI-vision guided cobots with quick-change 3D-printed tooling, they reduce changeover time from days to hours. The system uses sensor data and PLC commands to automatically reconfigure tasks. This solution directly addresses labor skill shortages while boosting overall equipment effectiveness (OEE).

FAQs: The Physical AI Up-Cycle

Q1: What exactly is “Physical AI”?

A1: Physical AI refers to the integration of artificial intelligence into robots and automated systems, enabling them to perceive, learn from, and interact with the physical world autonomously, beyond pre-programmed tasks.

Q2: Why are labor shortages driving automation now?

A2> Demographic shifts and a sustained high number of manufacturing job openings have created a structural labor gap. Automation, particularly flexible robotics, is no longer just for efficiency but a necessity to maintain production capacity.

Q3: Are humanoid robots the main focus of this trend?

A3> Not primarily. While they capture attention, the broader industrial up-cycle is driven by practical automation—collaborative robots, mobile platforms, and AI-enhanced existing machinery that solve specific cost and productivity challenges.

Q4: What is the biggest technical hurdle for next-gen robots?

A4> Advanced manipulation and dexterity. Improving “robot hands” with sophisticated tactile sensing and adaptive grip is crucial for expanding into complex assembly, logistics, and irregular object handling.

Q5: How should a business start preparing for this shift?

A5> Begin with a capability audit. Identify processes constrained by labor availability or complexity. Pilot a scalable AI-automation project, prioritizing partnerships with vendors that offer strong integration support and focus on system interoperability and data security.

No products in the cart.

No products in the cart.